To a relatively quiet last week, on Thursday, February 10 after the latest US inflation data was published, consumer prices grew by 7.5%, while core inflation reached 6.0% (against 5.5% a month earlier). Both values are the highest for the last 40 years, and this has not been observed since 1982. And it scared the markets.

Traders are worried that the US Central bank would act even more aggressively than expected to reduce inflation. The probability that the Federal Open Market Committee will raise interest rates by 50 basis points in March has jumped to 80%. There have also been rumors that the rate could be raised as many as seven times in 2022. Market analysts at Goldman Sachs predict that federal borrowing costs could rise to 2.0% by early 2023.

Looking forward for next week, Eurozone GDP data will be published on Tuesday, February 15. Elevated volatility can be expected due to the release of the next portion of data on the US consumer market the next day, on Wednesday, February 16. The publication of the February FOMC meeting minutes will also cause unconditional interest on this day.

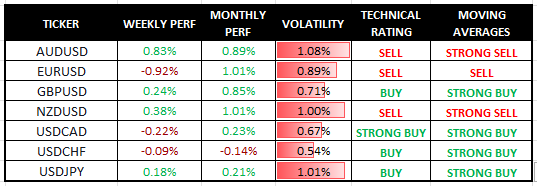

Major Currencies Performance and Signals

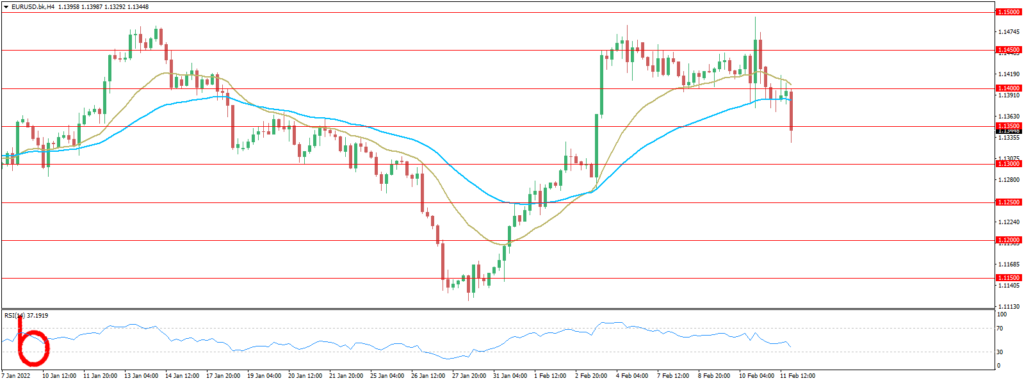

EUR/USD

Euro weakened last week due to hawkish Fed and geopolitical tensions with the Russia-Ukraine situation, EURUSD is at risk to escalation. Eyes on US data too, FOMC minutes in focus amid hawkish Fed

FORECAST: NEUTRAL

Resistance: 1.1350, 1.1400, 1.1450

Support: 1.1300, 1.1250, 1.1200

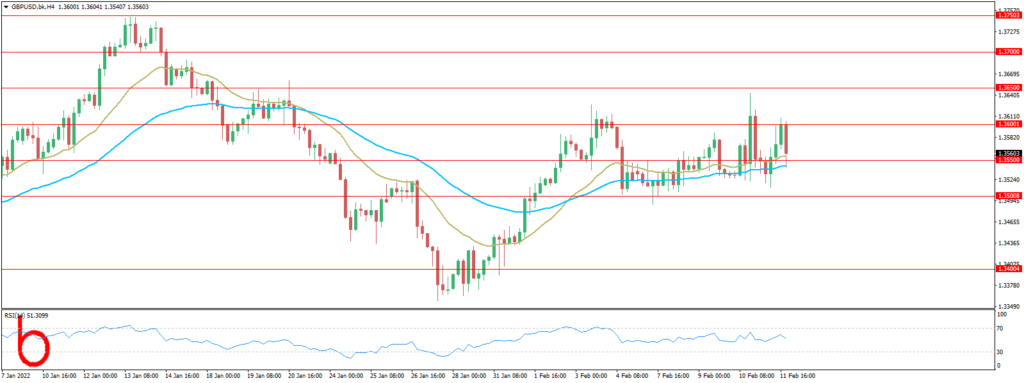

GBP/USD

The Pound rose by 0.24% to end the week at 1.3560. It’s a busy week ahead on the economic calendar. On Tuesday, claimant counts, and the UK’s unemployment rate will be key ahead of retail sales figures due out on Friday.

FORECAST: BUY

Resistance: 1.3600, 1.3650, 1.3700

Support: 1.3550, 1.3500, 1.3450

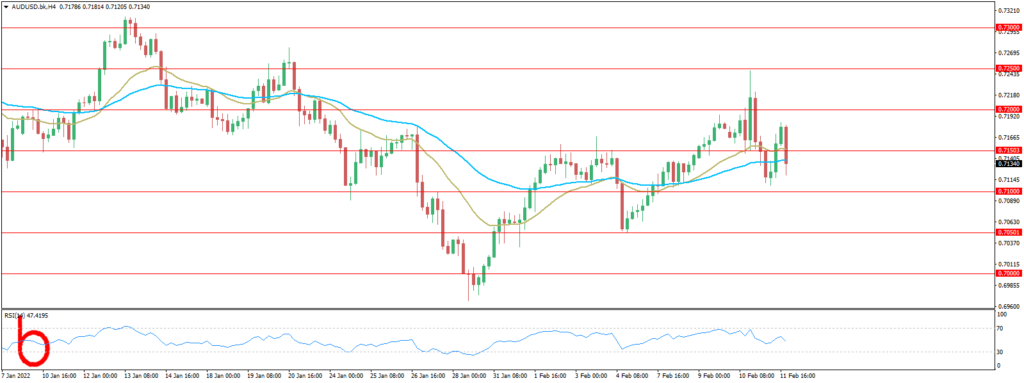

AUD/USD

The Aussie Dollar rose by 0.92% to 0.7137. It’s a quiet week ahead and the markets will need to wait for employment figures on Thursday. With the RBA holding back from any talk of rate hikes, positive numbers would be needed to force the RBA to shift its outlook. On the monetary policy front, the RBA meeting minutes on Tuesday will be key early in the week.

FORECAST: NEUTRAL

Resistance: 0.7150, 0.7200, 0.7250

Support: 0.7100, 0.7050, 0.7000

USD/JPY

The Japanese Yen fell by 0.14% to end the week at ¥115.420 against the US Dollar. It’s a fuller week ahead with the 4th quarter GDP, trade data, and inflation figures will be key stats in the week. Expect the GDP and trade data to have the greatest influence.

FORECAST: BUY

Resistance: 115.50, 116.00, 116.50

Support: 115.00, 114.50, 114.00

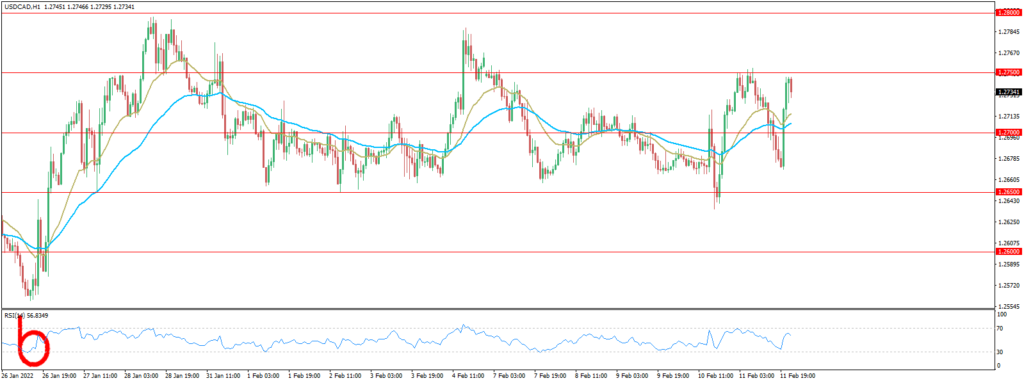

USD/CAD

The Loonie ended the week down to 1.2734 against the US Dollar. Early in the week, wholesale inflation and retail sales figures for January will draw plenty of interest and on Thursday, the focus will then shift to the weekly jobless claims and Philly FED manufacturing numbers.

Through the week, expect any FOMC member chatter to also draw interest. On the monetary policy front, the FOMC meeting minutes on Wednesday will also draw more interest than usual.

FORECAST: NEUTRAL

Resistance: 1.2750,1.2800, 1.2850

Support: 1.2700, 1.2650, 1.2600

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.