Last week the major currency pairs saw an appreciation against the US dollar except the Japanese Yen. The US Federal Reserve raised its interest rates for the first time since 2018, signaling more increases on rates to restrict raging inflation. US economic data continued to show resilience through February, with another jump higher in housing starts. Retail sales also showed people spending more on dining out, boding well for the expected pick up in services spending.

Oil prices were down last week as renewed lockdowns in China raised worries about demand. Uncertainty on the outlook is very high given Russia’s war in Ukraine, and we have marked down our own economic forecast released this week.

In addition to the ongoing situation in Ukraine, the focus next week will be also on the Fed speech, with Powell speaking on both Monday and Wednesday. The Fed has signaled a much stronger appetite to combat inflation, suggesting a further 6 rate increases in 2022. Looking at the comments from some of the Fed member that have spoken, there is a likelihood that we may even see a 50 basis point increase in May.

In the economic data front, the highlights include the US durable goods orders on Thursday and housing market data. From the UK, we have CPI and retail sales, while in Switzerland, the SNB will be making a “decision” on interest rates. Another set of key data will be the latest PMI numbers, due on Wednesday from Eurozone. On Monday, Japanese banks will be closed in observance of Vernal Equinox Day.

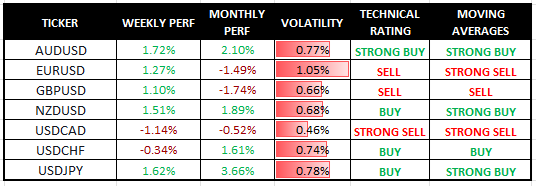

Major Currencies Performance and Signals

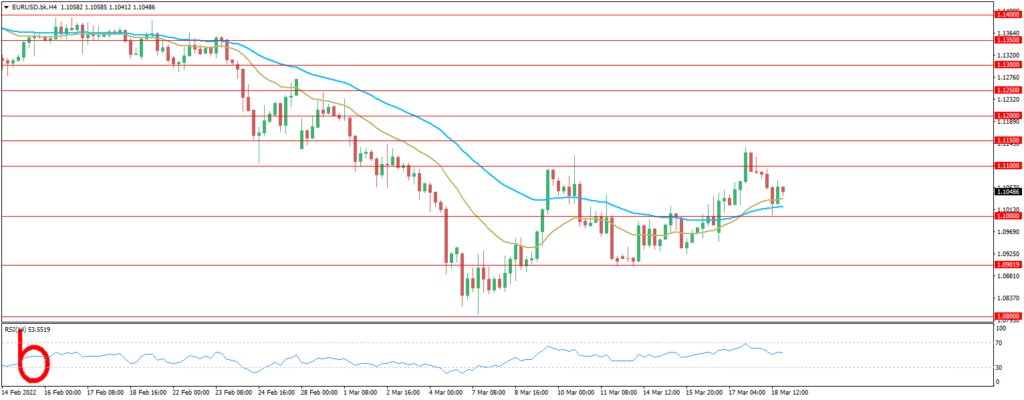

EUR/USD

The Euro has rebounded last week but next week based on the growing risks and the current outlook ahead, we see a bigger risk of a new weakening in market conditions with the US dollar set to advance vs the European currencies.

FORECAST: SELL

Resistance: 1.1000, 1.1050, 1.1100

Support: 1.0950, 1.0900, 1.0850

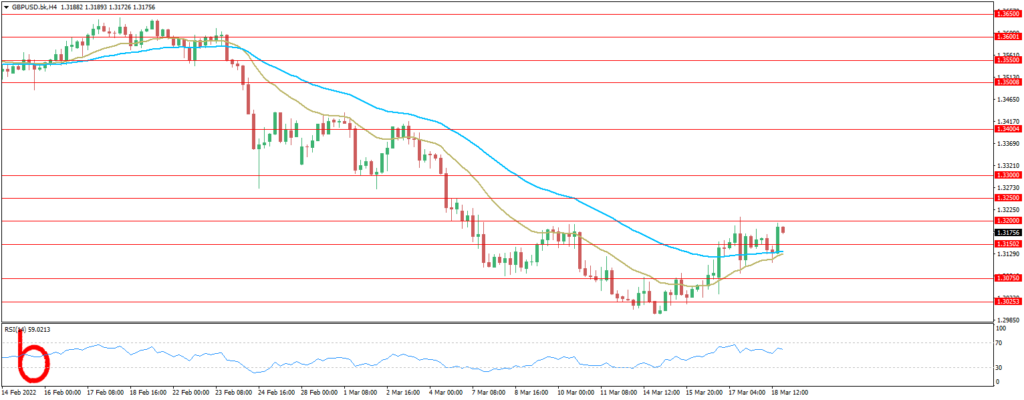

GBP/USD

Same situation as the Euro, the British pound has rebounded as well versus the US |Dollar. We expect that the GBP will go down due to continued risks and no resolution in the horizon of the Russian-Ukrainian war.

FORECAST: SELL

Resistance: 1.3200, 1.3250, 1.3300

Support: 1.3150, 1.3100, 1.3050

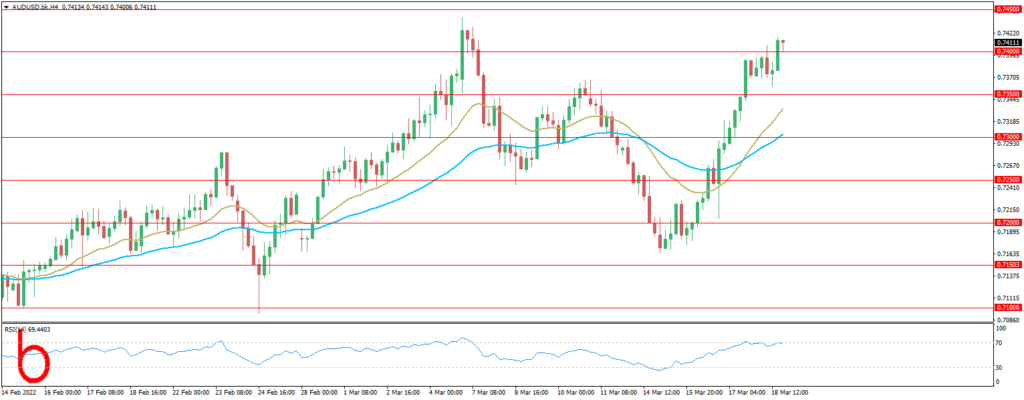

AUD/USD

Last week the Australian Dollar climbed to a four-month high after Chinese authorities pledged to support the economy. The Australian job report topped market expectations, strengthening the case for RBA rate hikes. We expect next week to continue the positive trend.

FORECAST: BUY

Resistance: 0.7450, 0.7500, 0.7550

Support: 0.7400, 0.7350, 0.7300

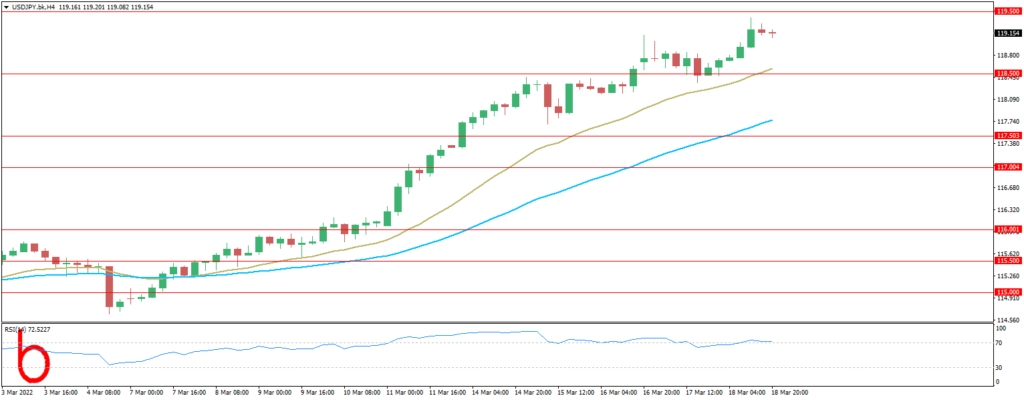

USD/JPY

The USDJPY last week has jumped above 118 as markets price in Japan’s soaring imported energy bill and the widening US/Japan interest rate differential. We expect next week to continue the positive trend.

FORECAST: BUY

Resistance: 119.50, 120.00, 120.50

Support: 119.00, 118.50, 118.00

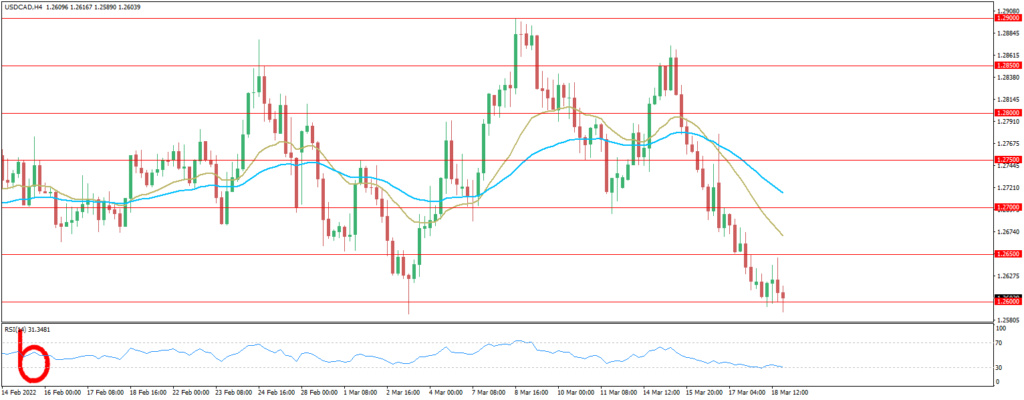

USD/CAD

The Canadian dollar has regained along with other risk assets, with USDCAD down more than 1.1% in the last five sessions. After this week’s pullback, USD/CAD is now sitting above a key support zone near 1.2600/1.2580.

FORECAST: SELL

Resistance: 1.2650, 1.2700, 1.2750

Support: 1.2600, 1.2550, 1.2500

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.