Last week, it was huge for stocks with a massive move showing up after the Fed’s rate hike on Wednesday. The FOMC hiked rates by 75 basis points and the S&P 500 jumped up to a fresh six-week-high. That move continued on Thursday and into Friday trade, helped along by an earnings report from Amazon on Wednesday afternoon and Apple on Thursday.

Next week, all eyes will be on the next Non-Farm payrolls report. For July, the economy is seen adding 250k positions, with unemployment sticking to 3.6%. A minor slowdown is seen in average hourly earnings, with a 4.9% year per year outcome expected from 5.1% prior. These are still healthy estimates and will likely contrast with the Fed pivot markets are anticipating.

The most important economic data for next week will be as follows:

- A quiet Monday this week with Swiss stock market will be closed in observance of Swiss National Day. Later in the day the US ISM Manufacturing PMI will be announced.

- Tuesday the Australian RBA Policy Announcement will be released and later the US JOLTS for June.

- Early Wednesday the New Zealand’s Employment Change and rate will be released. Later the Switzerland’s Consumer Price Index will be released, and later the US ISM Services PMI.

- Thursday will be an important day for UK as they BOE Monetary Policy Report will be released.

- Early Friday, the Australian RBA Monetary Policy Statement will be released. Later the most important number of the month the US and Canadian NFP employment Change and rate will be released.

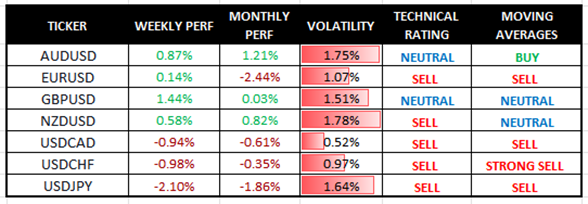

Major Currencies Performance and Signals

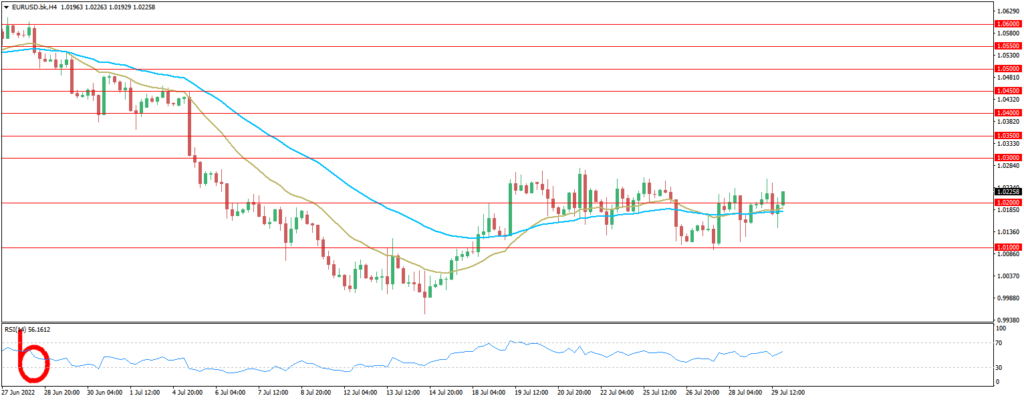

EUR/USD

The Euro slightly rallied as the US Dollar weakened this past week. Markets continue to favour a Fed pivot despite 75-bps rate hike. All eyes are on the US labour market and we are Neutral this week.

FORECAST: NEUTRAL

Resistance: 1.0250, 1.0300, 1.0350

Support: 1.0200, 1.0150, 0.0100

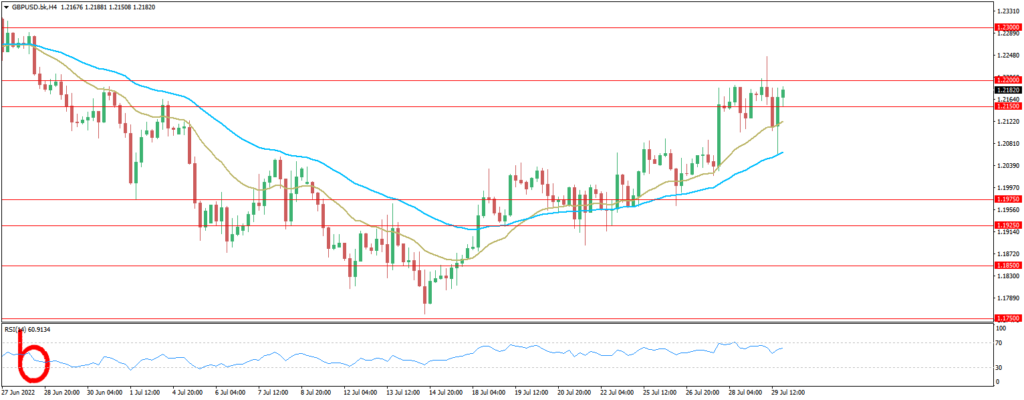

GBP/USD

The GBP/USD rallied significantly last week to reach above the 1.22 level, only to turn around and fall. All eyes on the NFP numbers next week but we remain bearish on the pair.

FORECAST: NEUTRAL

Resistance: 1.2200, 1.2250, 1.2300

Support: 1.2150, 1.2100, 1.1950

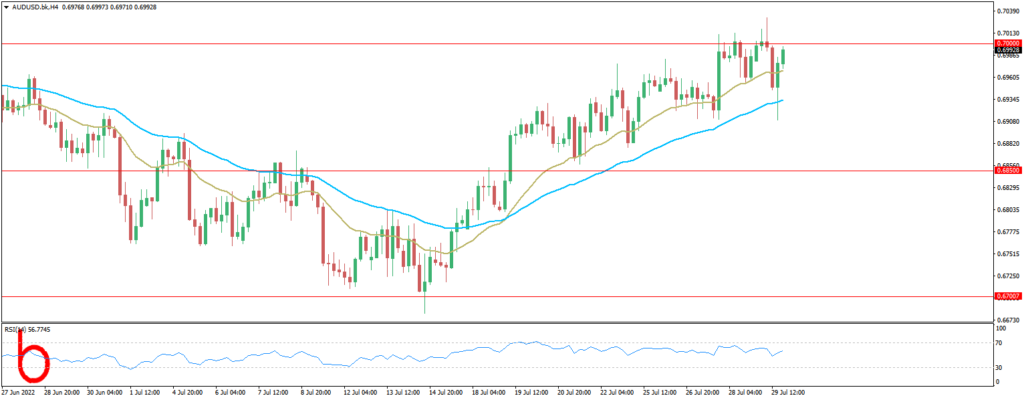

AUD/USD

The pair closed the week higher after Australia’s inflation rose to 6.1%, which markets expect will push the RBA to raise interest rates further in August. Next week our Aussies forecast is bullish as the Reserve Bank of Australia is expected to respond to rising inflation with a 50bps rate hike.

FORECAST: NEUTRAL

Resistance: 0.7000, 0.7050, 0.7100

Support: 0.6950, 0.6900, 0.6850

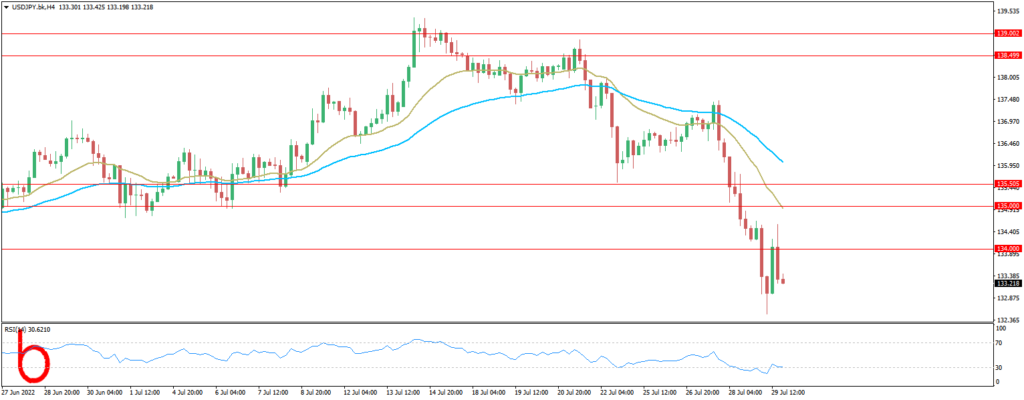

USD/JPY

USDJPY has continued to move lower as the narrowing of yield differentials and softer economic data limits Dollar strength. We are bearish on the USDJPY pair.

FORECAST: SELL

Resistance: 133.50, 134.00, 134.50,

Support: 133.00, 132.50, 132.00

USD/CAD

The pair depreciated for the second week as the US GDP report showed the US economy in a technical recession, and the weakening outlook for growth may continue to produce headwinds for the Greenback as it puts pressure on the FOMC to slow its hiking cycle. All eyes on the NFP results next week but we remain neutral on the pair.

FORECAST: SELL

Resistance: 1.2850, 1.2900, 1.2950

Support: 1.2800 1.2750, 1.2700

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.