Recessions have gone from being a potential consequence of high inflation and rapid monetary tightening to an increasingly likely scenario. Central banks are pushing back less and less against a period of negative growth, with Fed Chair Powell last week acknowledging it is “certainly a possibility”.

Investors are looking for any indication that inflation has peaked and is on a fast and sustainable direction lower, enabling central banks to take the foot off the gas and avert too much damage to the economy. We may have to wait a while longer yet.

Wall Street will continue to focus on the strength of the US consumer and pay close attention to personal income/spending data, another set of inflation readings, and a few key corporate earnings from the major retailers. A series of economic datais expected to confirm the trend of weakening business activity. US consumer confidence is expected to publish a strong decline, as personal incomes strive to keep up with inflation.

Next week, Monday starts with the G7 Meetings which will certainly give us some talking points throughout. The most important economic data releases next week will be as below:

• On Monday the US will publish its monthly Durable Goods Orders and Pending Home Sales.

• Early Tuesday the ECB President Lagarde will Speak and then the US will release its CB Consumer Confidence and Richmond Manufacturing Index.

• On Wednesday the German monthly Prelim CPI will be released and later the US quarterly Final GDP figure. Later we will have speeches from ECB President Lagarde Speaks, BOE Gov Bailey Speaks and Fed Chair Powell Speaks.

• Thursday a series of low impact releases around the day with the most important the US Core PCE Price Index and Unemployment Claims but also the Canadian monthly GDP figure.

• A quiet Friday with Canadian banks will be closed in observance of Canada Day but in the afternoon the US ISM Manufacturing PMI will be announced.

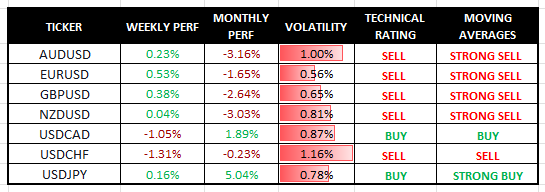

Major Currencies Performance and Signals

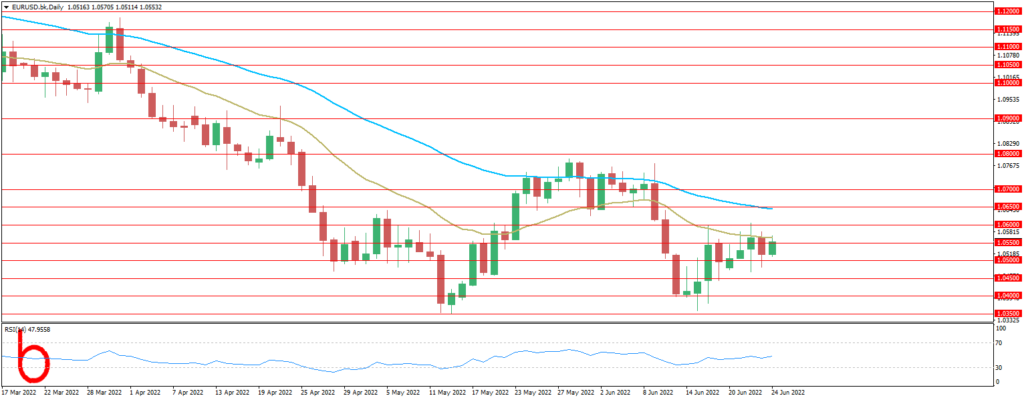

EUR/USD

The euro has displayed much resilience against the US dollar last week particularly after weak eurozone PMI figures.Nevertheless the momentum is still looking down and we are still bearish this week.

FORECAST: SELL

Resistance: 1.0600, 1.0650, 1.0700

Support: 1.0550, 1.0500, 1.0450

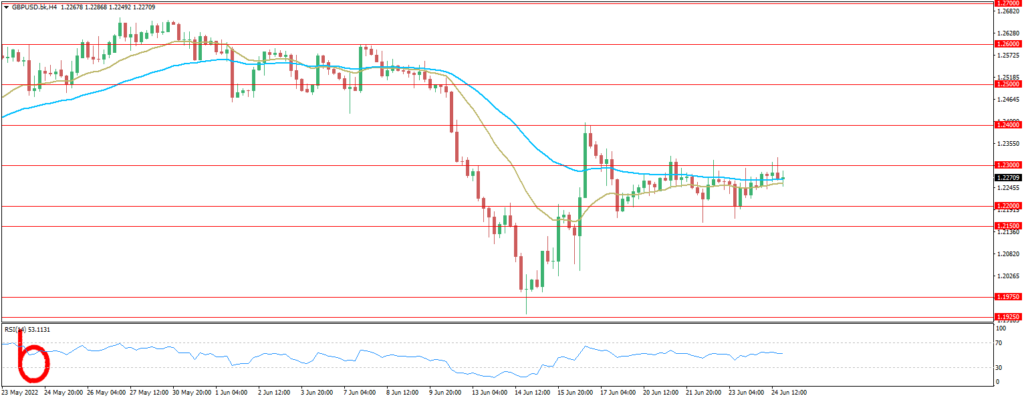

GBP/USD

The pound had some rather tricky data prints to route this last week with UK inflation and retail data alongside Jerome Powell’s two-day testimony.We expect the pair to be bearish this week.In the absence of positive GBP catalysts in the week ahead, there will be little to spur Cable higher, apart from a weaker dollar. We are bearish this week.

FORECAST: SELL

Resistance: 1.2300, 1.2350, 1.2400

Support: 1.2250, 1.2200, 1.2150

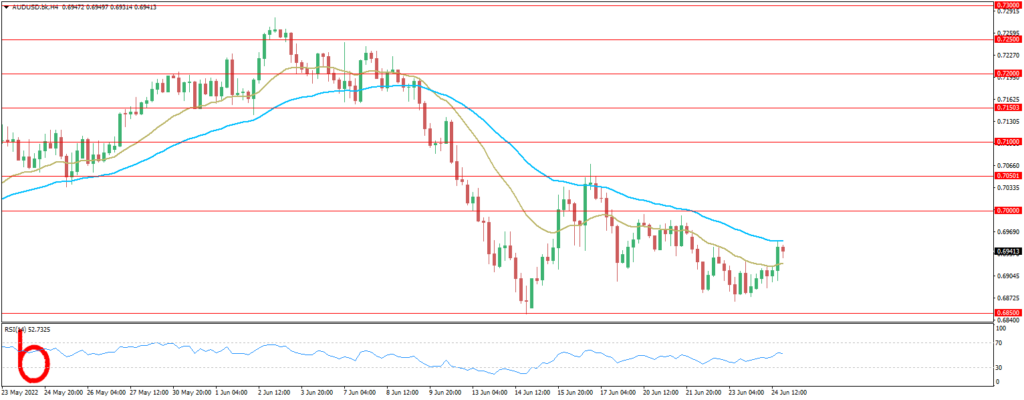

AUD/USD

Australian Dollar price swings echoing evolution of global recession fears.Growth forecasts fade amid inflation fight, China lockdowns, Ukraine war. G7, NATO and ECB summits compete for influence with top data ahead.We are bearish on the pair.

FORECAST: SELL

Resistance:0.7000, 0.7050, 0.7100

Support:0.6950, 0.6900, 0.6859

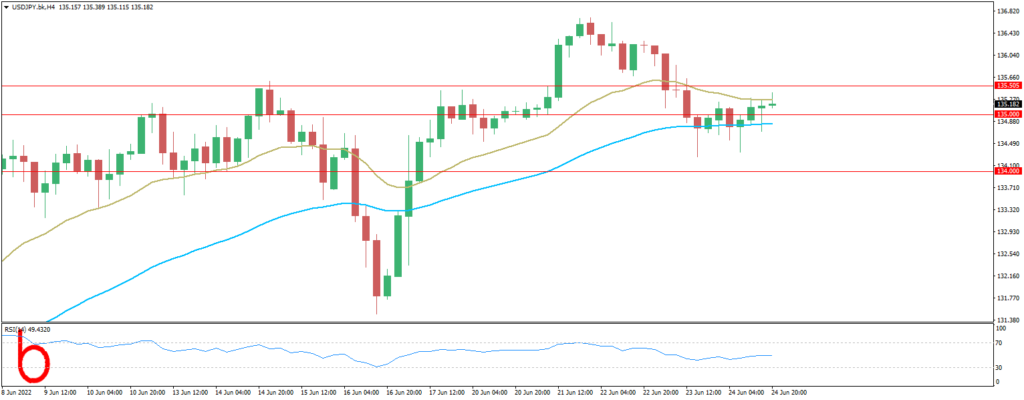

USD/JPY

USD/JPY remains highly volatile and entirely correlated to the US/Japan interest rate differential. We may still be a long way from Bank of Japan intervention. We continue to be bullish on the pair.

FORECAST: BUY

Resistance: 135.50, 136.00,136.50,

Support: 135.00, 134.50, 134.00

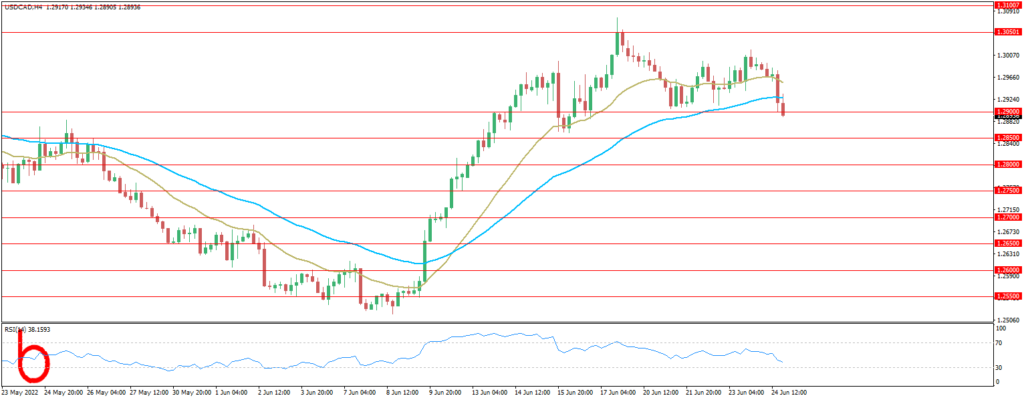

USD/CAD

Canada’s politicians criticize the Bank of Canada for failing to control inflation.A lot of domestic data from the US could cause volatility for USD/CAD in the coming week. We are bullish for this week.

FORECAST: BUY

Resistance: 1.2900, 1.2950, 1.3000

Support: 1.28501.2800, 1.2750

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.