Last week, a strong dollar has been a hot topic since the software giant Microsoft and Salesforce Inc. CRM, pointed to challenges the currency is causing for earnings. It’s been identified in other industries too, including by Pfizer Inc., eBay Inc., and MasterCard since foreign sales can be hurt by a US Dollar.

A strong US dollar will make it more expensive for American companies to sell their goods on the international market, which hurts the stock market. But cheaper imports from a robust dollar help US consumers, the driving force of the economy, particularly as households face high costs for gas, groceries and more.

The European Central Bank is set to flag its first-rate hike in more than a decade this week, while the Reserve Bank of Australia might step on the brakes harder. But as the laggards of the central bank world finally get their stakes on when it comes to tightening policy, investors will be on the lookout for more evidence that inflation may already be peaking in the United States.

Next week on the economic data front it is expected to be a quiet week with some important news coming out of Europe, Australia, and the US.

On Monday, the market will be quiet as German, French, Swiss and New Zealand banks will be on holidays. Tuesday most important figure will be the Australian RBA Rate Statement. On Thursday the ECB interest rate decision will be made with the markets expecting the ECB to leave rates unchanged, the focus will be on ECB President Christine Lagarde and the press conference. Lastly, on Friday the Canadian Employment Change and the US CPI numbers will take center stage.

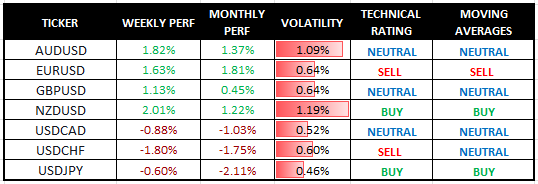

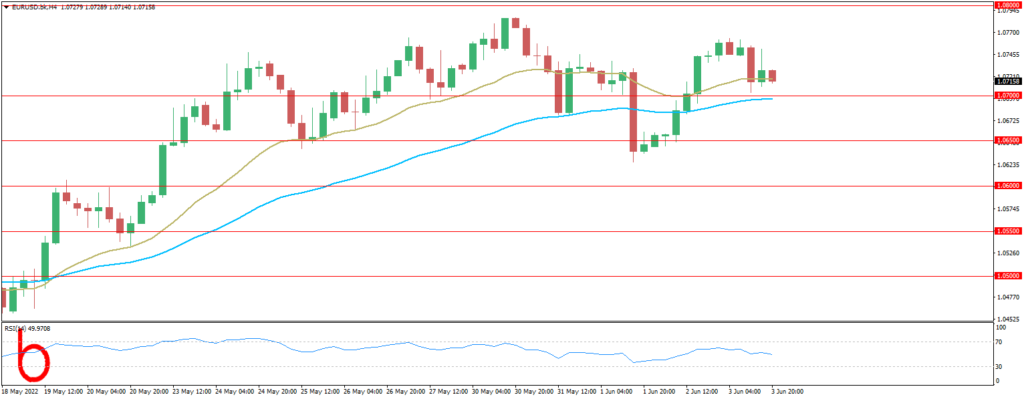

EUR/USD

In the previous week, the EUR rallied by 1.62% to $1.0735. A quiet week ahead but expected to be impactful on Thursday where the Monetary Policy Statement will be expected to hike. We expect the pair to be bearish.

FORECAST: SELL

Resistance: 1.0750, 1.0700, 1.0750

Support: 1.0700, 1.0650, 1.0600

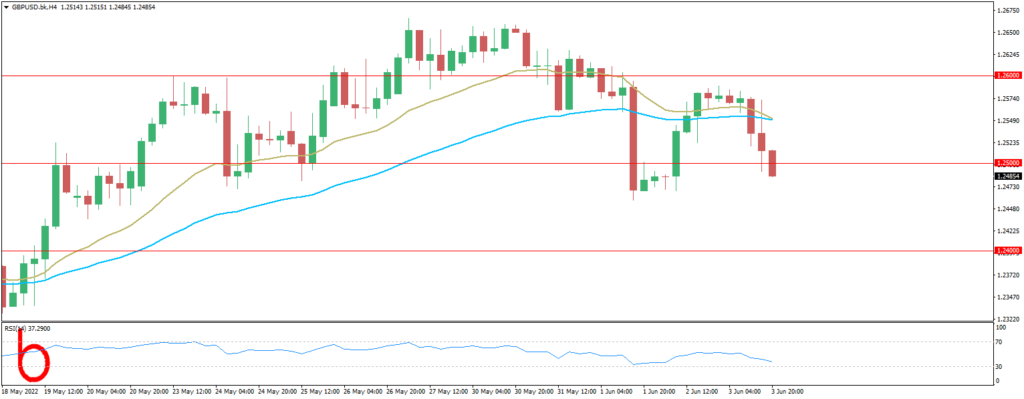

GBP/USD

The British Pound rose by 1.21% to $1.263 in the week prior. BRC Retail Sales Monitor numbers for May are due out on Tuesday along with finalized private sector PMIs. Any revisions to the services PMI will have the greatest impact on the Pound. We expect the pair to be bearish.

FORECAST: SELL

Resistance: 1.2500, 1.2550, 1.2650

Support: 1.2450, 1.2400, 1.2350

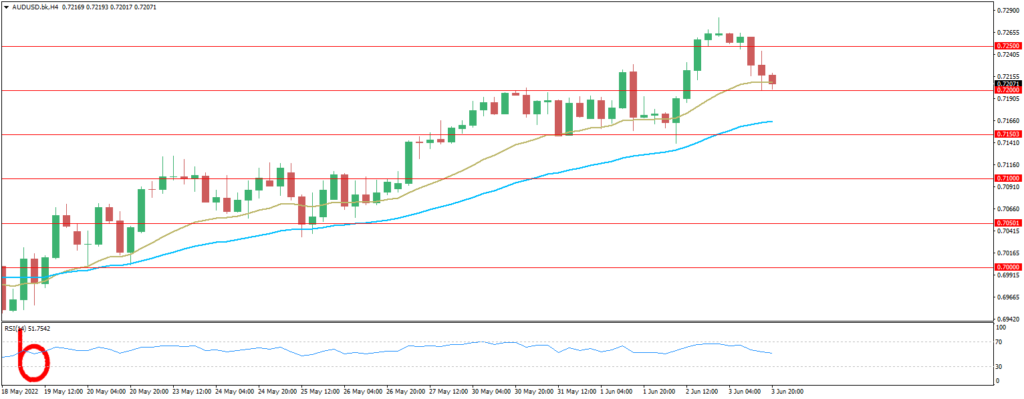

AUD/USD

This week, the main event will be the RBA’s June monetary policy decision on Tuesday. The markets are expecting a 25-basis point hike. Anything more and a hawkish rate statement would support an Aussie Dollar breakout. We are NEUTRAL on the pair.

FORECAST: NEUTRAL

Resistance: 0.7250, 0.7300, 0.7350

Support: 0.7200, 0.7150, 0.7100

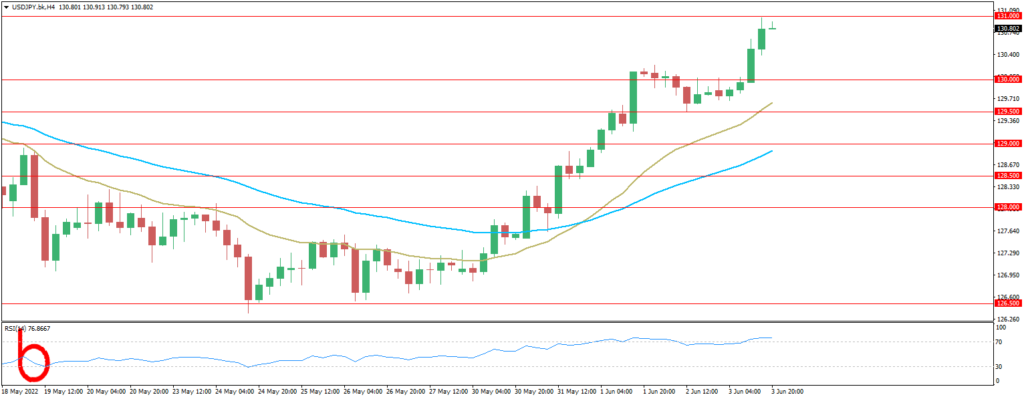

USD/JPY

Last week, the US Dollar appreciated further vs the Yen as the greenback was strengthened. On Tuesday, household spending will draw interest ahead of first quarter GDP numbers due out on Wednesday. We are bullish on the pair.

FORECAST: BUY

Resistance: 131.00, 131.50, 132.00,

Support: 130.50, 130.00, 129.50

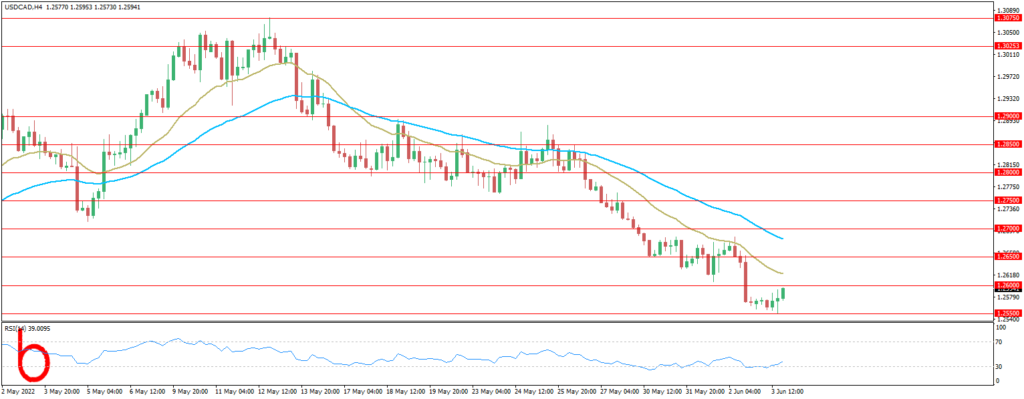

USD/CAD

For the Loonie, the main event, will be the employment figures for May. We expect the pair to continue its bearish trend.

FORECAST: SELL

Resistance1.2600, 1.2650, 1.2700

Support: 1.2550, 1.2500, 1.2450

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.