The July Fed meeting was a catalyst for global financial markets. Ditching its forward guidance, the FOMC has now moved to a data dependent stance. Fed Chair Jerome Powell didn’t do much to push back on market expectations that we’re on the other side of peak Fed hike expectations, and rates markets continue to discount rate cuts in 2023.

Forward looking measures of inflation indicate that peak inflation is in the rear-view mirror, and the 2Q’22 US GDP report indicated that the economy is slowing (recession or not, there’s no reason to quibble over the technical definition). These facts bring a more dovish Fed moving forward, whereby even if there are more rate hikes, they’re unlikely to be at the same 75-bps pace we’ve seen over the past two meetings.

These are expected to translate into a weaker US Dollar, or at least a US Dollar that’s less likely to continue its meteoric rise moving forward. But primarily, these developments mean that US real yields are likely to fall back in the near-term.

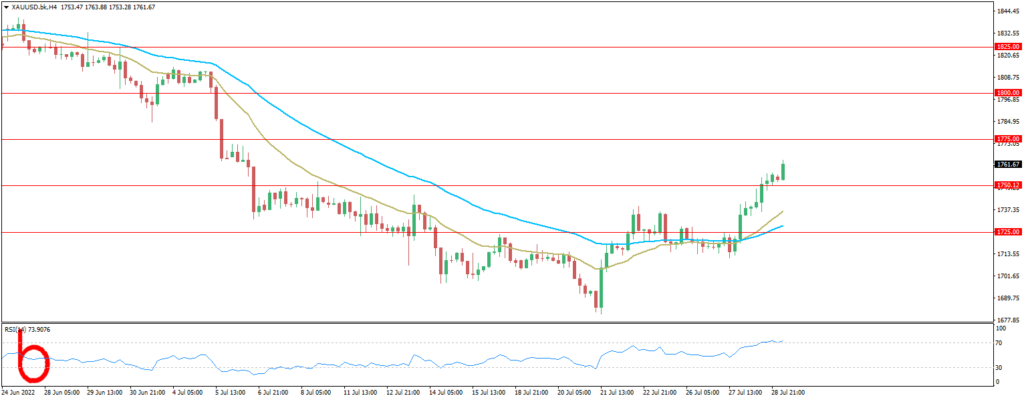

If there was any question about how much of a catalyst this is for precious metals, just look at how silver prices have performed: the gold/silver ratio has collapsed from a high of 93.61 on Monday to as low as 87.93 today (-6.07% this week alone).

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.