Bears on the US Dollar drove the dollar Index -0.5% lower on Thursday. This followed a drop in Treasury yields that totally undone yesterday’s rise sparked by FOMC minutes, which hinted at the threat of Fed tapering. Broad US Dollar weakness sent EUR/USD ripping 50-pips higher to test yearly open resistance while USD/JPY tumbled -0.41% on the session. The DXY Index now hovers back at a key area of technical support near the 89.65-price level.

Looking ahead to Friday’s trading session on the Economic Calendar, we see significant event risk caused by the scheduled release of PMI surveys by IHS Markit. However the overnight US Dollar implied volatility readings suggest that major currency pairs are likely to have comparatively a small movement.

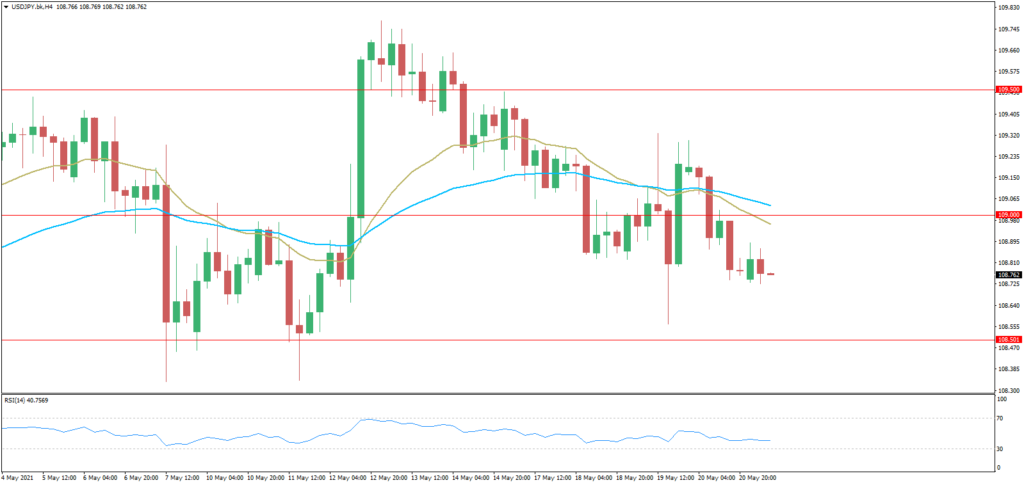

USDJPY overnight implied volatility of 4.5% is below its 20-day average reading of 5.5% and ranks in the bottom 20th percentile of readings over the last year. If US PMI data stresses constant supply chain disruptions and corresponding price pressures, however, currency volatility could accelerate alongside a sharp spike higher in Treasury yields as markets grow more fearful of inflation and the risk of Fed tapering.

We remain short on the USDJPY.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.