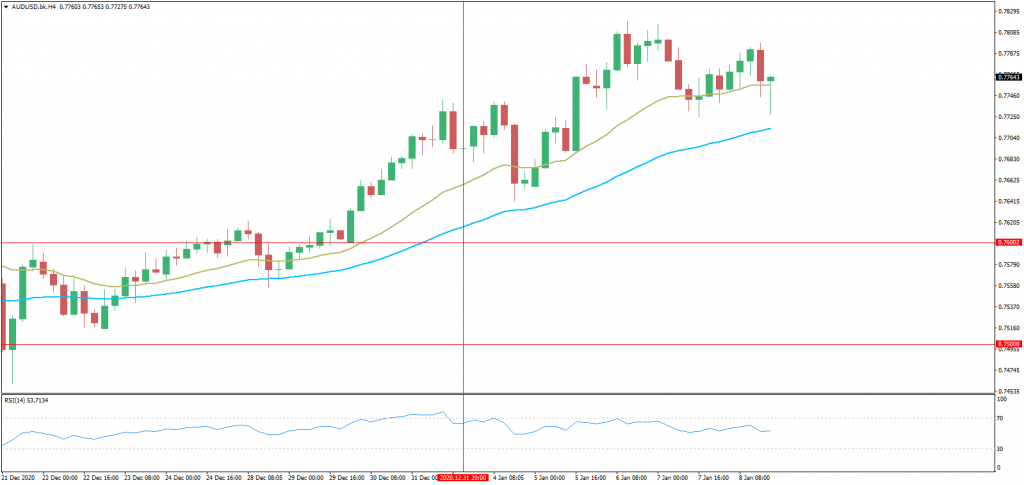

Last week, the AUD/USD continued to gain throughout the week until Friday which there were a small selloff with a bounce back.

At the moment, the pair struggles to recover the ground lost early Monday despite the upbeat Aussie data released soon before press time.

As shown by Retail Sales, consumer spending in Australia rose 7.1% month-on-month in November following October’s 7% rise. The Melbourne Institute’s inflation data showed the cost of living in Australia rose by 0.5% month-on-month in December following November’s 0.3% rise.

The Aussie pair still trades at session lows below 0.7700, representing a 0.64% drop on the day. The US dollar looks to be benefitting from the recovery rally in the Treasury yields. The 10-year yield jumped over 20 basis points to 1.12% last week and is currently seen at 1.11%.

“As yields rise, they may be triggering foreign hedges or other flows that put a bid in the dollar,” Adam Button, Currency Analyst at AhsrafLaidi.com, noted, adding that a continued rise in yields would eventually work against equities and provide a significant tailwind for the dollar.

The pair, however, may find some support later today if China’s Producer Price Index for December prints above zero, marking an end of a multiple month-long deflationary trend in factory-gate prices.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.