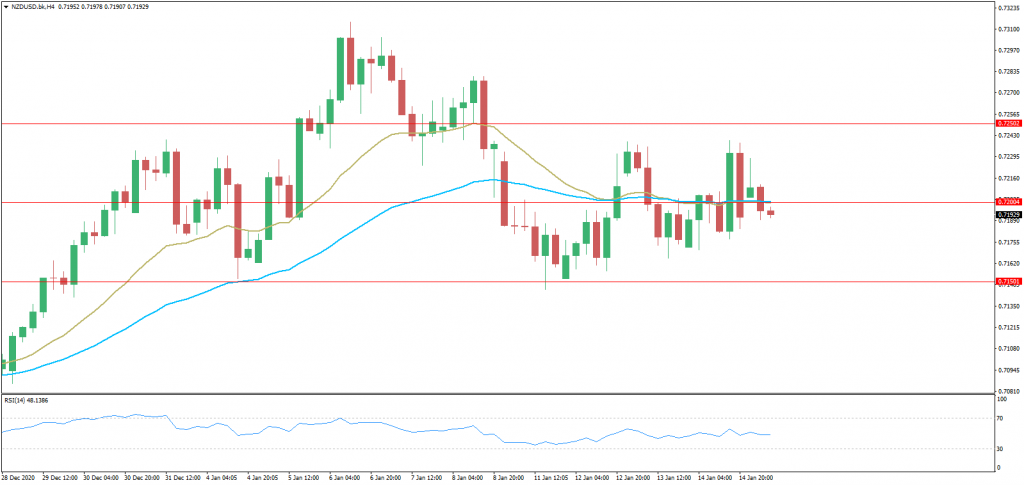

NZDUSD has been a bit in the background in recent trade, dropping back from close to session highs in the upper 0.7230s to current levels around 0.7220 and remaining well supported above 0.7200. The pair closed on Thursday, with decent gains amid a broadly softer US dollar, rising 0.6% or 46 pips.

The US dollar weakened mainly against its more risk sensitive G10 peers on Thursday in the run-up to comments from the Chairman of the Federal Reserve Jerome Powell, who largely fixed to the usual dovish script on Fed policy and on the topic of asset purchase program tapering, pushed back against the notion that this is going to happen, or indeed should be talked about, soon.

Moderate weekly jobless claims data out of the US might have also added to weakness in the currency; in the week ending on the 9 January, 965K American signed up for unemployment insurance, a substantial spike from the week prior’s 784K reading and well above expectations for 795K. The numbers show that after a rough December for the US labor market (as indicated in last week’s official NFP report), weakness has spilled over to January, which is unsurprising given the rate at which Covid-19 is spreading in the country is yet to relent and many industries (namely hospitality and leisure) are still locked down.

Traders will await to hear from incoming US President Joe Biden on the fiscal stimulus plan he will push for once he gets into office, though many details have now been released.

Technically, the pair broke above key trendline resistance on Thursday; the pair broke above a downtrend linking the 6, 8 and 13 January highs to rally back to match the previous weekly high at 0.7240. The pair has now retraced for a retest of this downtrend and it is holding up as support for now.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.