Last week, the US equity record highs seemed to boost the Aussie. Australian macroeconomic figures continue to indicate economic growth. The AUDUSD pair has a rang to bearish bias, and break below April lows should signal a steeper decline.

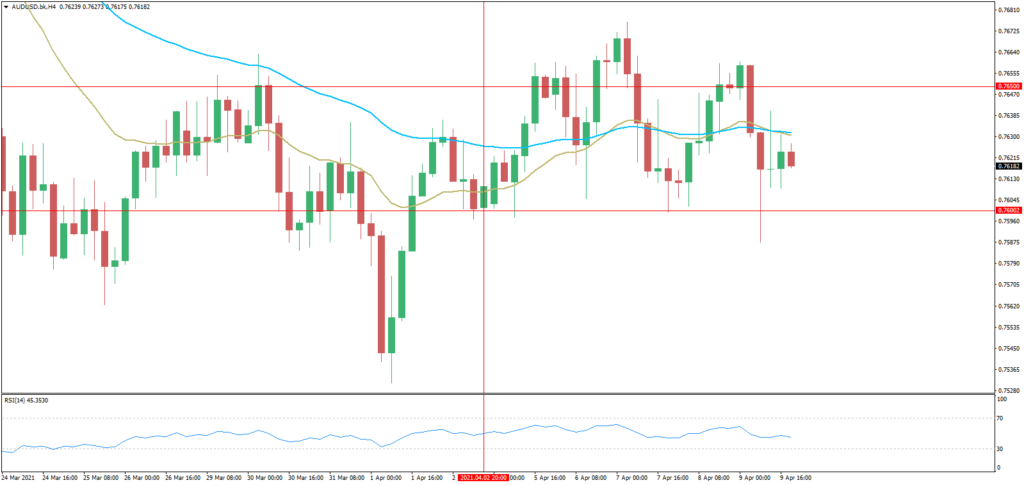

The AUDUSD pair closed with small gains around 0.7620 and has been hovering within an 80 pips range for six days in a row, bottoming on Friday at 0.7587. Reduced demand for the US Dollar and stronger equities fell short of boosting the pair, in some way expecting additional drops in the future. Also, declining metal prices, with gold retreating from weekly highs, added additional pressure on the Aussie.

Technically, the Aussie is currently walking below the neck of a head-and-shoulders pattern. Not only is price up against the neck-line of the formation, but also trading at a trend-line off the high (H&S head). This confluence of resistance makes the next move crucial.

On the economic data front, the Australian macroeconomic calendar included the March AIG Performance of Services Index, which printed at 58.7, better than the previous 55.8. The country will not release macroeconomic figures this Monday, while China will unveil money-related data and their GDP which also is expected to have a narrow impact on currencies.

We remain Neutral this week on the Aussie.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.