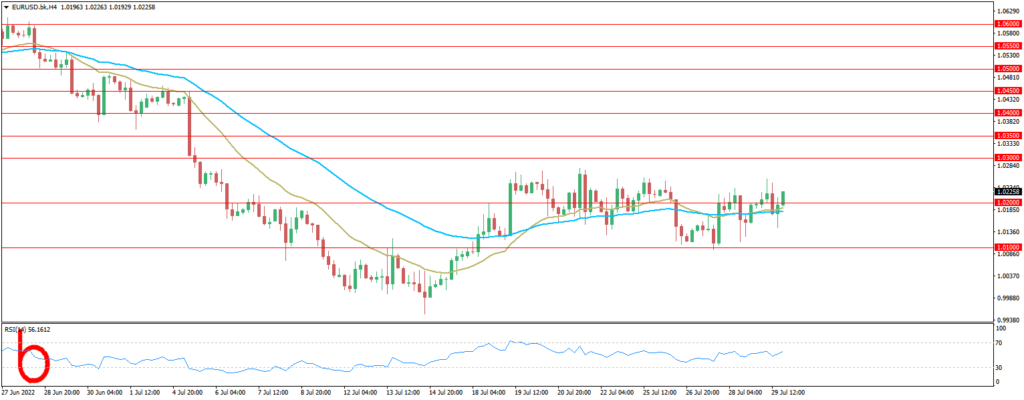

The Euro moved just higher against the US Dollar this past week. That appears to be largely a result of general weakness in the US Dollar. The Euro-Area economic data is rather thin in the week ahead, so the focus on EUR will likely depend on external factors. In this case, it might make sense to look at what is going on in the United States. Although, it should be noted that the European Central Bank has been pushing out increasingly hawkish commentary as of late. But, as we will see, it still pales in comparison with the Fed.

Inflationary data this past week continued to show that the Fed has a problem to tackle. The Employment Cost Index, which is the central bank’s preferred wage gauge, surprised higher at 1.3% q/q in Q2 versus 1.2% seen. Meanwhile, the Fed’s ideal inflation gauge also beat estimates.

In the week ahead, all eyes will thus be on the next NFP report. For July, the economy is seen adding 250k positions, with unemployment sticking to 3.6%. A minor slowdown is seen in average hourly earnings, with a 4.9% y/y outcome expected from 5.1% prior. These are still healthy estimates and will likely contrast with the Fed pivot markets are expecting. As such, remain vigilant. Volatility can still return, opening the door for a US Dollar reversal, therefore pressuring the Euro.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.