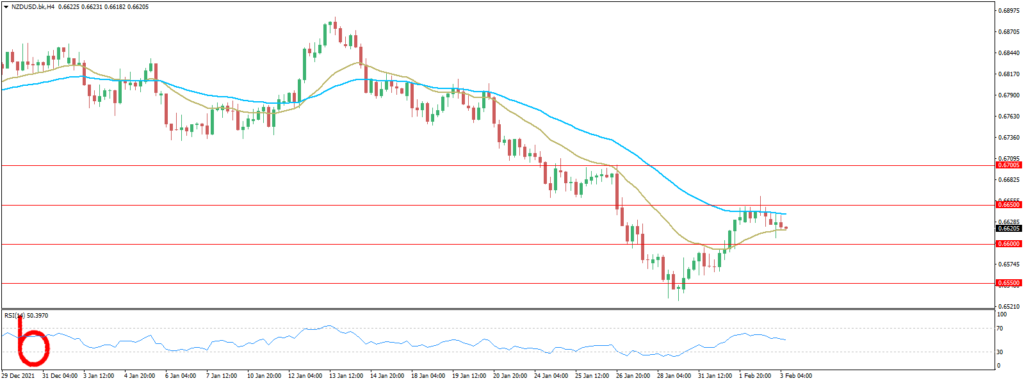

The Kiwi climbs but moved back from weekly highs around 0.6662 after mixed than foreseen NZ jobs report released in the Asian session. At the time of writing, the NZDUSD is trading at 0.6637.

An hour and a half before Wall Street’s opened, the ADP Jobs report was released. The figures were dismal, showing the losses of more than 301K employments when polled economists expected at least 207K private jobs added to the economy.

The ADP Chief Economist said that “The labor market recovery took a step back at the start of 2022 due to the effect of the Omicron variant and its significant, though likely temporary, impact to job growth.” Nevertheless, officials in the White House and Fed members warned that the January employment report would be disappointing, subject to the impact of the Omicron variant.

For the moment, in the Asian session, New Zealand’s employment report showed that the unemployment rate fell from 3.3% to 3.2%, while the Labor Cost Index jumped two tenths from the previous month to 2.6%., but short of the 2.9% foreseen.

The RBNZ is expected to hike rates 25 basis points to the Overnight Cash Rate (OCR) at the February meeting. Nevertheless, wage growth is lagging widely, so the NZ central bank could decide to slow rate hike increases in 2022, allowing inflation to shoot up.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.