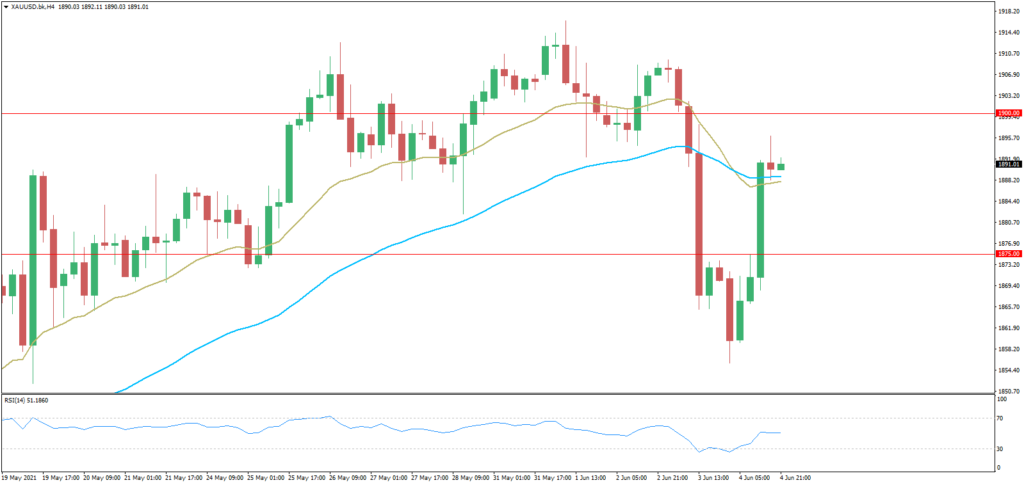

Last week the yellow metal aimed lower, cutting some downside progress on Friday. A worse than expected US non-farm payrolls report sent Treasury yields and the US Dollar lower, offering XAU/USD some upside momentum. Whilst average hourly earnings beat expectations, the headline jobs gain was measured at 559k, lower than the 650k consensus. While the unemployment rate dropped, so did the labor force participation rate.

The most important event risk for gold next week is the Thursday’s US CPI report. The core inflation rate, which strips out volatile food and energy prices, is anticipated to show 3.4% yearly in May. On the chart below, that would be the most since early 1993, or just about 30 years ago. An unexpected beat in the data could revive Fed tapering bets, pushing up bond yields, the US Dollar and bringing down anti-fiat gold prices.

Even though the extent of follow-through may have to wait until the next Fed interest rate decision later this month. Some members, such as Patrick Harker, have begun alluding to talking about when to unwind lose policy. The central bank’s position, for now, is that recent inflation is temporary, being impacted by a low support effect from a year ago.

By itself, it could be possible that expectations ahead of the central bank leaves gold in a consolidative state. Traders may await how the Fed could change its tone amid last week’s NFPs and the upcoming CPI report. On Friday, the University of Michigan sentiment is expected to make things more complex at 84.0, up from 82.9 prior.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.