The US Dollar closed on Thursday almost flat judging by the DXY Index. The US Dollar price action was mixed across the board of major currency pairs with trends against the Yen largely make up for weakness versus the British pound. Treasury yields rose for the second day in a row with the ten-year extending its rebound off Wednesday’s swing low to 5.4-basis points. Bond yields stayed perky even after strong demand was seen for today’s $62-billion seven-year Treasury auction.

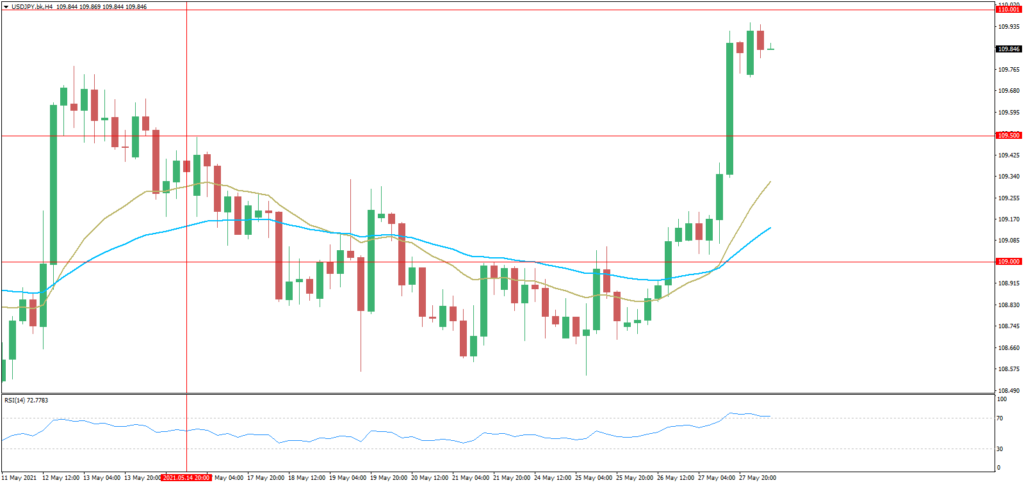

All the above likely helped push USDJPY to a new monthly high, though the bid questionably looked worsened by a broadly softer Yen. Maybe news that the MSCI Global Standard Index is removing 29 Japanese listings weighed negatively on the Yen and positively on JPY-crosses. That said, the latest increase by the USDJPY pair seems to have canceled its bearish trendline as bulls wrestle back control.

In the Friday’s economic data schedule, we can see that high-impact risk is caused by the scheduled release of monthly PCE inflation data. This is the Fed’s favorite gauge of inflation and stands to have impact on markets.

We remain bullish on the USDJPY for today.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.