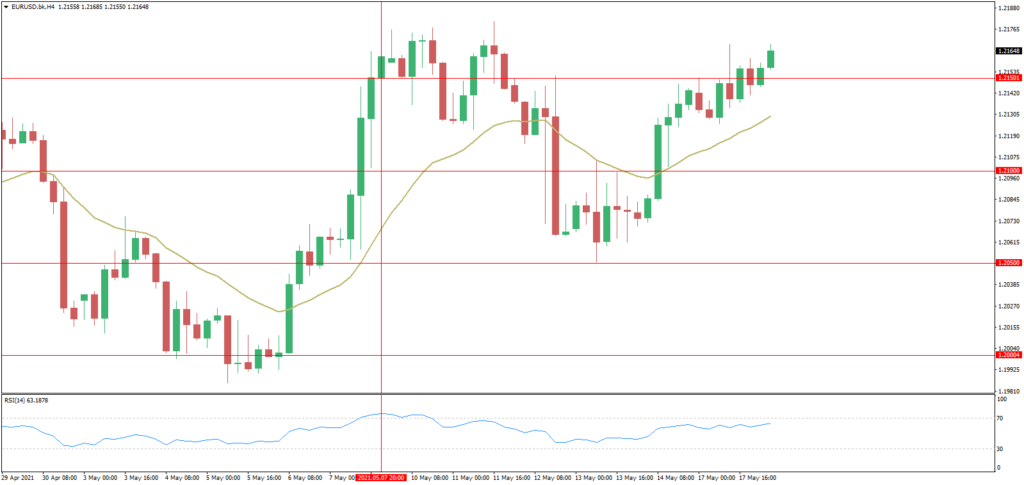

Last week, the Euro pair was volatile as the market mirrored the strong inflation data from the US. The data showed that consumer prices rose by 4.2% in April while the producer price index rose by 6.2% in the month. This increase was larger than what most analysts were expecting. It even stunned some Fed officials, including Vice President, Richard Clarida, who believes that the figure was temporary.

This week, the pair will react to the latest Eurozone GDP data that will come out today, Tuesday. Analysts anticipate that the numbers will show that the EU GDP declined by 0.6% in the first quarter, leading to a 1.8% year-on-year contraction. The figure will come a few days after the European Commission increased its forecast for the bloc. It expects the economy to bounce back by 4.2% in 2020 and by 3.8% in 2022.

The EURUSD will also react to the latest inflation data from the Eurozone that will come out on Wednesday. Based on the estimate released two weeks ago, analysts expect the data to show that the headline CPI rose by 0.6% on a MoM basis and by 1.6% on a year-on-year basis. The core CPI is likely to have risen by 0.6% on a YoY basis.

The EURUSD will be also affected by the latest data from the United States like housing starts, building permits, and initial jobless claims numbers.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.