The Aussie grew following a blowout jobs report for February. Australia added 88.7k positions against expectations of a 30k increase. The majority of these were drawn from the full-time sector (89.1k) as part-time shrunk 0.5k. Australia’s unemployment rate also edged down to 5.8% from 6.3% prior, marking the lowest point in almost one year. Economists were anticipating a hold at 6.3%. Participation held at 66.1%.

The AUDUSD rise on the employment report also follows the outcome of the FOMC interest rate decision. There, a rise in the Dow Jones, S&P 500 and Nasdaq pressured the US Dollar as the central bank reiterated its dovish stance despite improving economic projections. The Fed anticipates real GDP to rise 6.5% this year versus December’s 4.2% projection.

As such, we may see the Australian Dollar continue benefiting as Asia-Pacific and European markets follow Wall Street’s rosy lead in the remaining 24 hours. However, Fed Chair Jerome Powell’s continued calm about rising longer-term Treasury yields may offer some upside potential to the Greenback. These risks are forcing stocks that are perceived to be the most overvalued, such as those in tech, and thus cooling the Aussie.

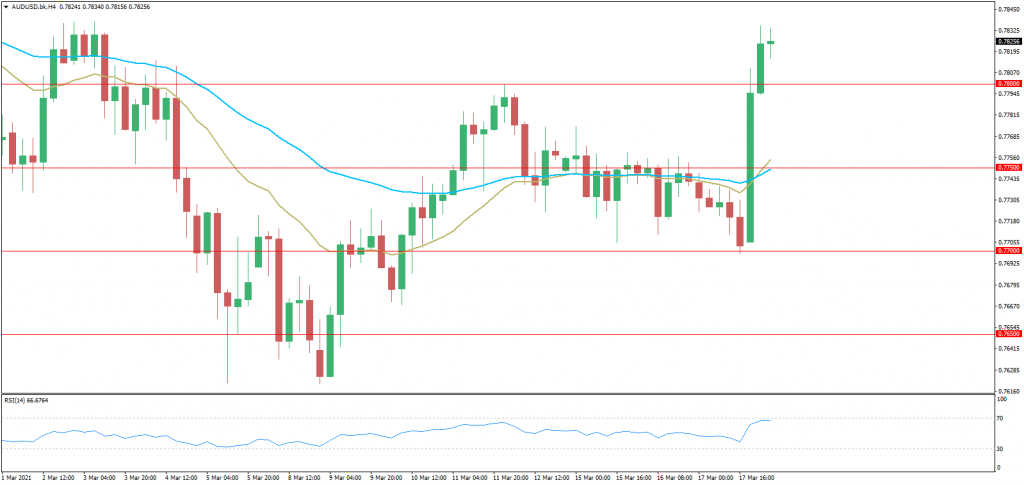

The pair possibly remains biased to the bullish side from a technical standpoint. Keeping the focus to the upside appears to be rising support from December and the 100-day Simple Moving Average (SMA). The latter is hovering around the 0.7564 – 0.7622 support zone, which may come into play in the event of a turn lower.

A drop through these points of critical support may open the door to reversing the major uptrend, towards the 0.7343 – 0.7413 inflection zone. On the other hand, confirming a break above the 0.7798 – 0.7820 inflection range exposes the February high at 0.8007.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.