Last Week, the Euro has made its largest weekly loss for nearly three months last Friday after consolidating previously at what were new year highs for the single currency. Only now the EURUSD pair may need a rally from either the Pound or Chinese Yuan to sustain a significant recovery.

There is not a lot on the US economic calendar next week that could surprise the market. The Philly Fed manufacturing gauge (Thursday), flash PMIs (Friday) and a barrage of housing data should provide an important update on the health of the US economy, though no one are expected to impact the market.

In Its place, the focus for traders will be on Wednesday’s inauguration proceedings for the new POTUS Joe Biden. The danger of violent marches appears ahead of what is normally a tradition for the financial markets. With President Trump’s supporters still falling to accept that the election result was fair and after the historic marching of Capitol Hill by rioters on January 6, renewed unrest could move markets, triggering some risk aversion, as it could be predicting of more insurgence to come.

This week is rich with impactful economic announcements from the main currencies. Monday’s Forex market is expected to have low volatility due to US banks being closed in observance of Martin Luther King Day.

The Chinese will report their fourth quarter GDP measure and flash PMIs along with inflation and retail sales numbers will be the talk of the town in most markets. Still, traders will once again be focus on the happenings on Capitol Hill in Washington amidst fears of possible violent attacks at Joe Biden’s inauguration and a potential vote in the Senate on Trump’s impeachment case.

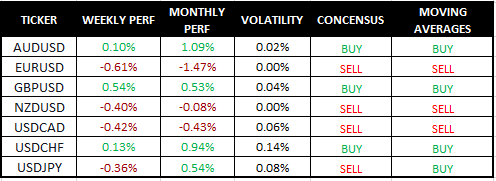

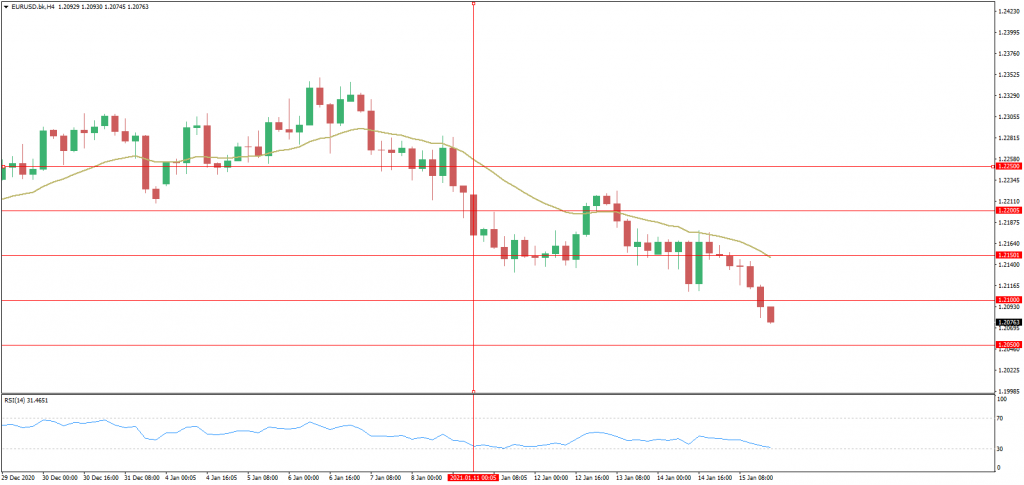

EUR/USD

Risk aversion looks to have entered through weekend with the S&P500 delaying to move higher despite President-elect Biden’s stimulus plan. The US Dollar broke higher with EURUSD sliding below 1.2150 – but it is not clear whether it was due to its relative growth or safe haven appeal.

Next week the top event risk looking ahead includes: China 4Q GDP; the Presidential inauguration; ECB and BOJ rate decisions; earnings and January PMIs.

FORECAST: LONG

Resistance: 1.2100, 1.2150, 1.2200

Support: 1.2050, 1.2000, 1.1950

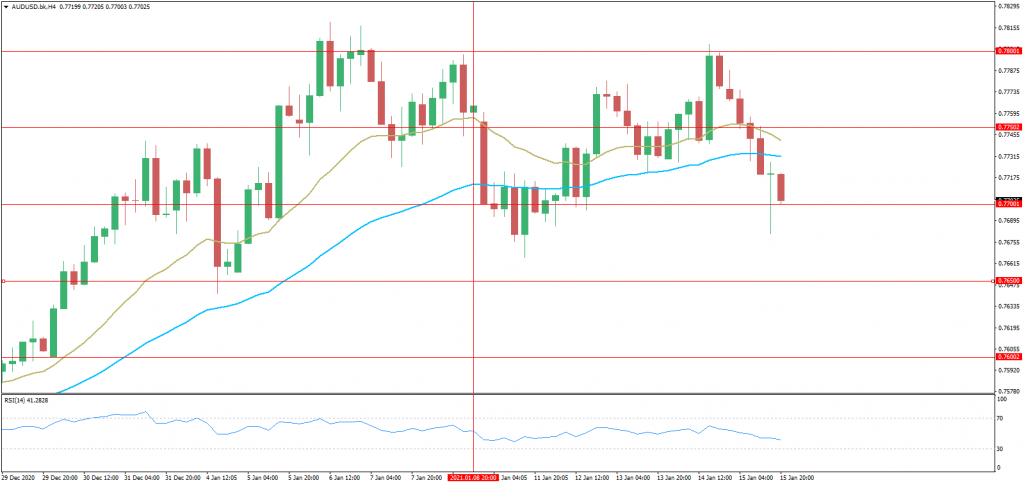

AUD/USD

The Aussie reached a near three-year high on Thursday. On Friday, the US Dollar gained despite dismal US Retail Sales, Jobless Claims. The Australia employment expected to continue recovery in December and commodity currencies retain strength as global recovery expected.

FORECAST: LONG

Resistance: 0.7750, 0.7800, 0.7850

Support: 0.7700, 0.7650, 0.7600

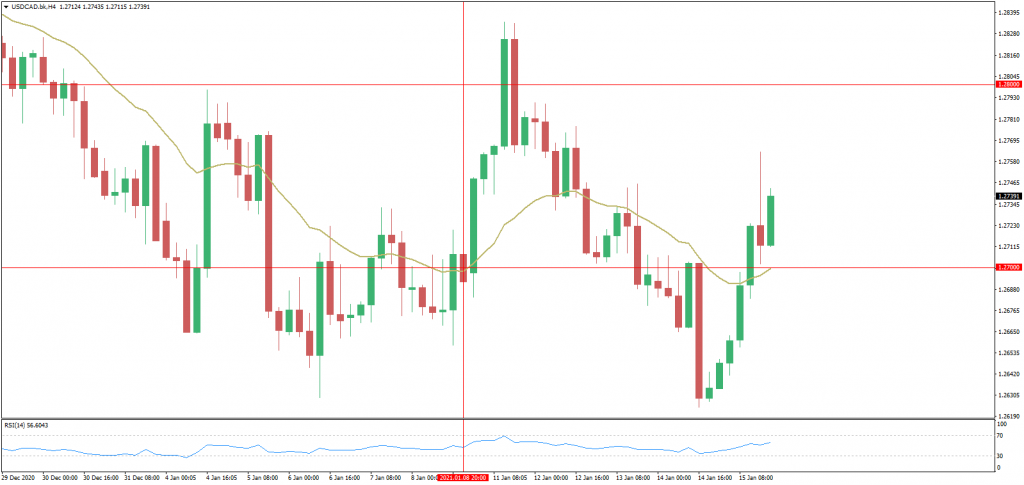

USD/CAD

From a big picture point of view, the current bounce back is a major disappointment for USD to CAD bears as the pair failed to settle below 1.2625 for the second time in January. We remain short.

FORECAST: SHORT

Resistance: 1.2800, 1.2850, 1.2900

Support: 1.2700, 1.2650, 1.2600

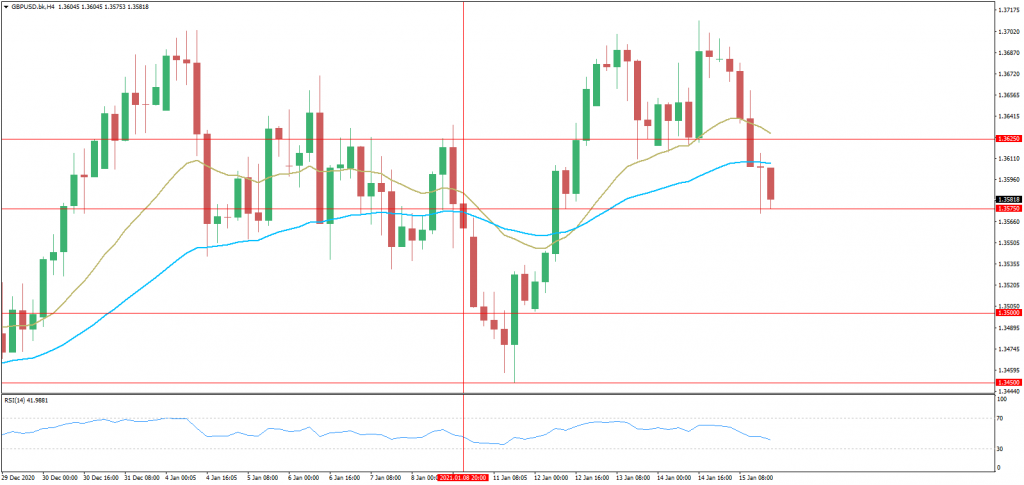

GBP/USD

Fitch Affirms the UK at ‘AA-‘ with the Outlook Negative as the UK’s ratings balance a high income, diversified and advanced economy against high and rising public sector indebtedness. The Negative Outlook reflects the impact of the coronavirus pandemic on the UK economy and the resulting material deterioration in the public finances, with Fitch estimating the fiscal deficit to have widened materially to 16.2% in 2020 and government debt set to increase to 120% of GDP over the next few years.

FORECAST: SHORT

Resistance: 1.3600, 1.3650, 1.3700

Support: 1.3500, 1.3450, 1.3400

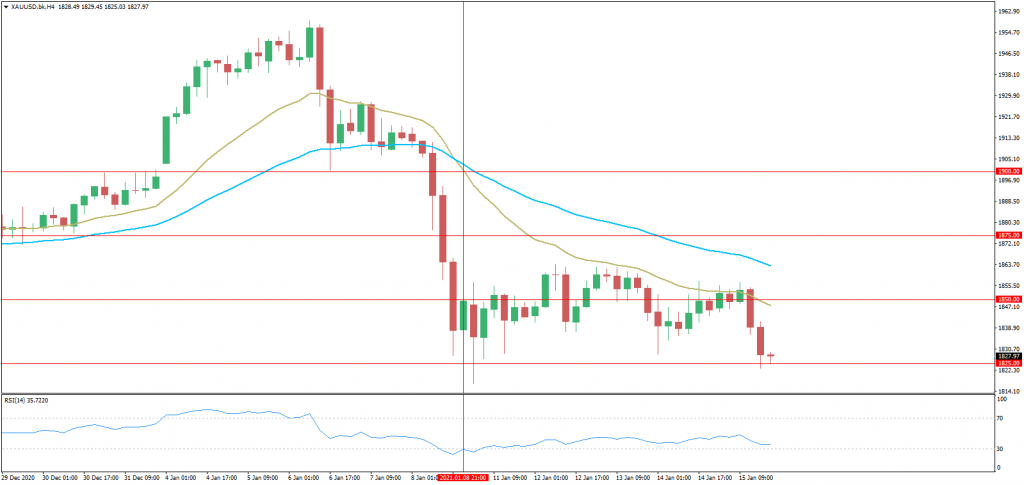

GOLD (XAU/USD)

Gold was fluctuating at a very tight range on Friday. The XAU/USD pair can push higher if it manages to break above 200-SMA on H4 chart. The key support for gold is located at $1,817.

FORECAST: SHORT

Resistance: 1850, 1900, 1950

Support: 1825, 1800, 1750

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.