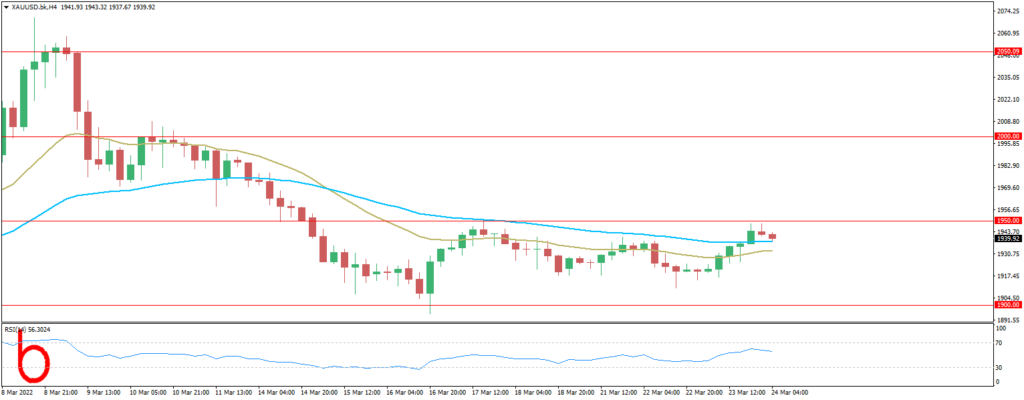

Gold praised the US Treasury yields decrease from three-year high the previous day to print notable gains. However, the bond coupons recover, underpinning the US dollar strength, amid the market’s anxiety ahead of the key data/events.

That said, S&P 500 Futures seesaws between gains and losses, up 0.11% intraday around 4,452 by the press time while the US 10-year Treasury yields retreated from a three-year high to 2.30% before regaining a 2.33% level at the latest.

The latest hawkish Fed speech highlighted the US PMIs for March and Durable Goods Orders for February. Also, the Ukraine-Russia tensions and the US readiness to slap more sanctions on Moscow emphasize President Biden’s meeting with the North Atlantic Treaty Organization (NATO) allies in Europe. Furthermore, China’s covid update and fears emanating from the Middle East also can challenge the gold prices on a key day.

Going forward for today, the economic calendar is full of mega-events on Thursday. US will reveal the Initial Jobless Claims, Durable Goods Orders, and Markit (Manufacturing and Services) PMI on Thursday. Nevertheless, the focus will remain on the EU leaders summit to discuss the embargo on Russian oil and US President Joe Biden meeting with his NATO counterparts to discuss the Russia-Ukraine hostilities and attitude for a diplomatic solution.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.