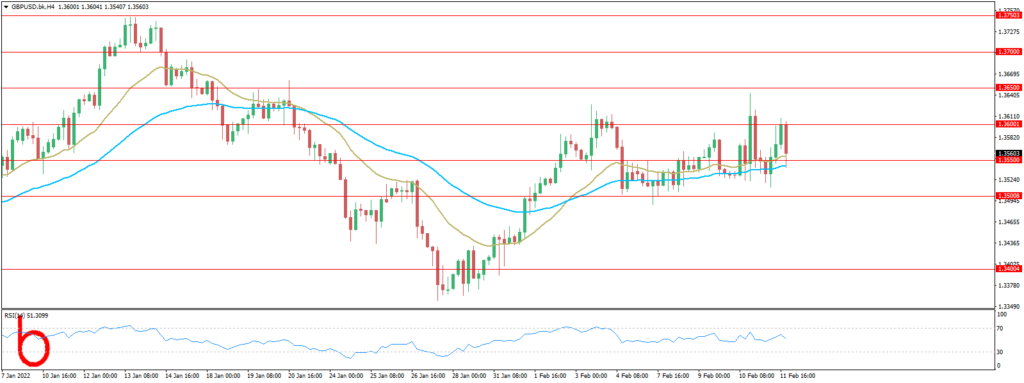

While the ECB is lagging the Fed, the Bank of England is so far ahead, raising interest rates faster than its peers across the Atlantic. Consequently, unlike the euro, the British pound managed to hold its ground so far last week, finishing the five-day period at 1.3551. The key word here is “so far”: “so far ahead” and “managed so far.” The superiority of the pound over the dollar is very wobbly and it can quickly start retreating.

The primary factors that could push the Bank of England to stop raising the rate, leaving it at a low level, are weak GDP and labor market growth, as well as low levels of consumer spending. According to the data published on Friday, February 11, the UK’s GDP, instead of the expected 1.1%, grew by only 1.0% in the Q4 2021. And the situation in the labor market and the consumer market will become known next week: statistics on the unemployment rate will be released on February 15, and that on the level of prices in the United Kingdom – on February 16.

The fact that this regulator will continue to act very carefully, which was confirmed by the Bank of England chief economist Hugh Pill. He said in an interview with Reuters that the bank expects “further moderate tightening in the coming months if everything goes as planned” and that “one needs to be careful in setting the rate level.”

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.