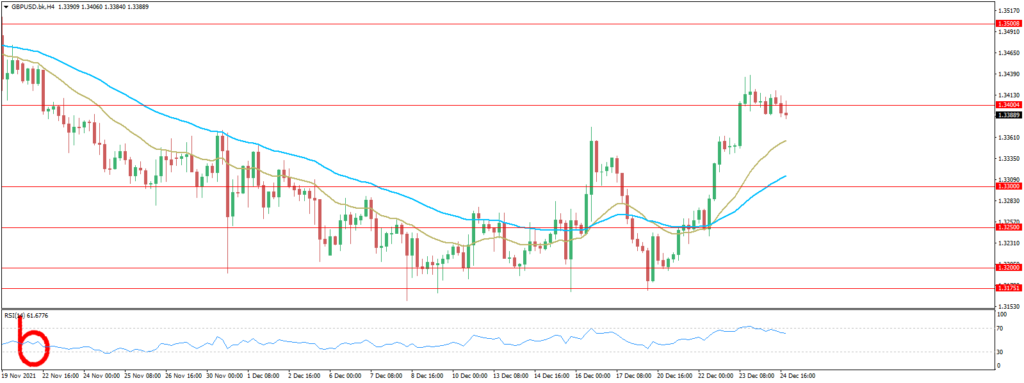

The British Pound initially got off a slow start last week, as sentiment was reduced by concerns over the rise in domestic Covid-19 cases and speculation the government will impose stricter restrictions to slow the spread of the Omicron variant.

The Cable then began to recover on Tuesday following the announcement from Boris Johnson that the government would not be imposing any new restrictions before Christmas. The Pound then dropped on Wednesday with the publication of the UK’s latest GDP figures after the third quarter’s finalized figures saw growth was revised lower, raising concerns that the UK economy was slowing even before the emergence of Omicron.

Looking forward to this week, the direction of the GBPUSD exchange rate will essentially depend on whether the UK government decides to impose tighter Covid restrictions. Should the government decide that stricter measures are necessary then Sterling is likely to tumble. Otherwise, the Pound may maintain a positive trajectory.

Meanwhile, the US Dollar may stumble if Omicron developments remain broadly positive. However, with most market participants off until the new year trade in the GBP/USD exchange rate is likely to remain exceptionally thin, likely limiting any major movement in the pairing.

Warning:

Trading on CFDs involves a high level of risk, including full loss of your trading funds. Before proceeding to trade, you must understand all risks involved and acknowledge your trading limits, bearing in mind the level of awareness in the financial markets, trading experience, economic capabilities and other aspects.

Disclaimer:

Market Trends, Charts, Trading Ideas or other information provided by BKFX (Pty) Ltd and/or third parties are not intended as an investment advice and/or recommendation. The information provided is not presented as suitable or based on your specific need. You are responsible for your own investment decisions and you should not trade with money you cannot afford to lose. Any views or opinions presented in this Article are solely those of the author and do not necessarily represent those of the Company, unless otherwise specifically stated. The Company may provide the general commentary which is not intended as an investment advice and must not be construed as such. Seek advice from a separate financial advisor if an investment advice is needed. The Company assumes no liability for errors, inaccuracies or omissions, inaccuracies or incompleteness of information, texts, graphics, links or other items contained within this article/material.